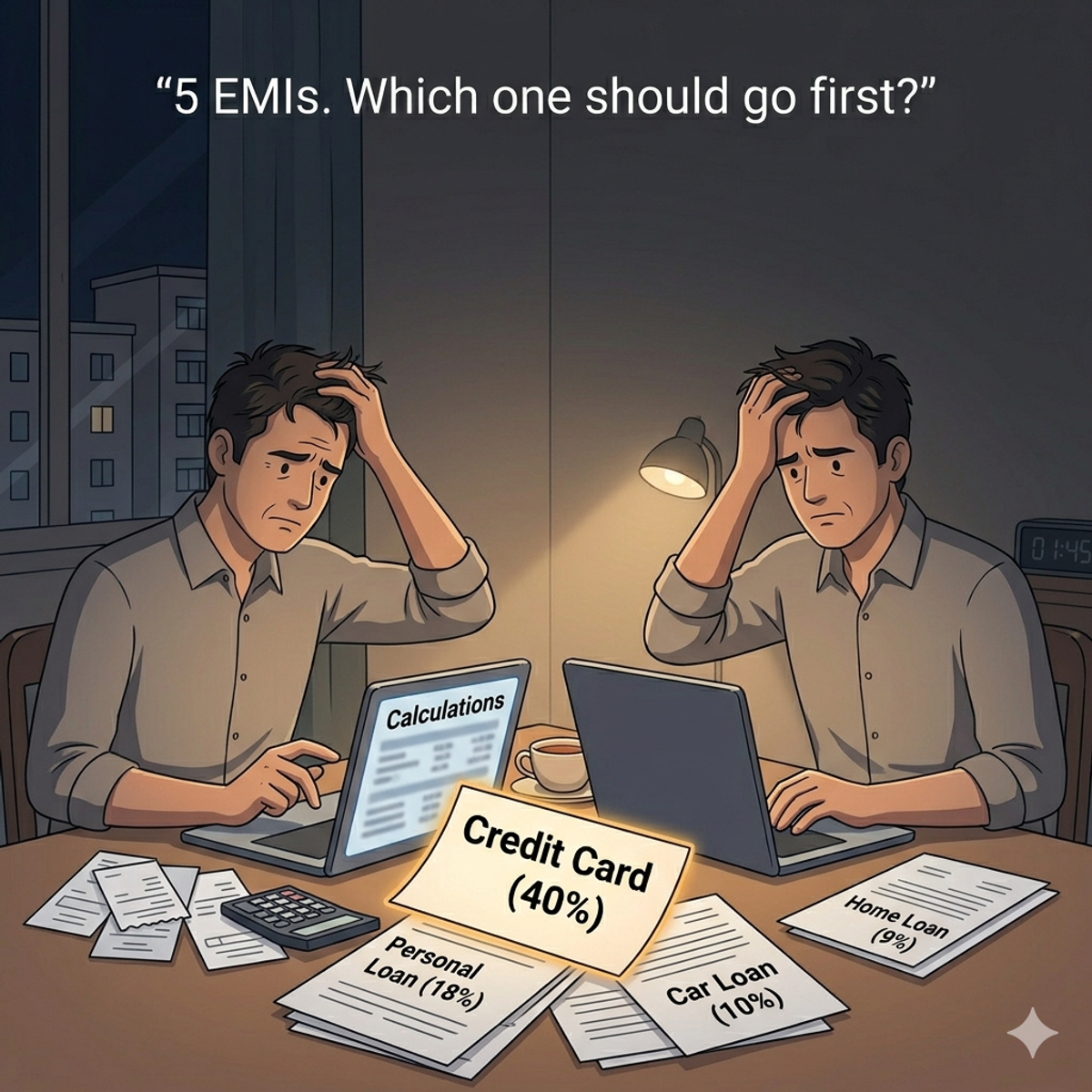

Figuring out which loan to pay off first? For most salaried Indians, the answer is to close the highest-rate debt first — credit cards charge 36–48% APR in India, versus 9% for a home loan. The order determines total interest paid, often by lakhs. Kedil consolidates all your EMIs in one view so you can see exactly which costs you the most.

Why the order matters

Not all debt is equal. A ₹1 lakh balance on a credit card at 40% APR costs you ₹40,000 per year in interest. The same ₹1 lakh on a home loan at 9% costs ₹9,000. Same rupee amount — 4x the interest cost.

According to RBI data, the average debt per borrower in India rose from ₹3.9 lakh in March 2023 to ₹4.8 lakh in March 2025. For most salaried professionals, that's spread across a home loan, personal loan, credit card, and possibly a car loan or BNPL balance.

The order you pay these down isn't just a math problem. Over a 10-year horizon, it's a decision worth lakhs.

The two strategies: avalanche and snowball

Avalanche method: Put any extra money towards the highest-interest loan. Make minimum payments on everything else. Once it's cleared, move to the next highest.

Snowball method: Pay off the smallest outstanding balance first, regardless of interest rate. The logic: clearing small debts quickly gives you wins that keep you on track.

Avalanche saves more money — always. Snowball gives quicker psychological wins.

For Indian debt stacks, where there's typically a 20–30% rate gap between credit card debt and everything else, the avalanche method wins by too wide a margin to ignore.

For most salaried Indians: close the credit card first

Credit cards are the most expensive debt most salaried Indians carry. APR ranges from 36% to 48% per year — three to five times more expensive than a home loan.

The practical decision order:

- Credit card balance — Pay this first. No exceptions.

- Personal loan (13–22% APR) — Close this second.

- Car loan (8–14% APR) — Third.

- Home loan (8.5–9.5%) — Make your regular EMI. Let it run.

Home loans also come with a tax benefit: interest up to ₹2 lakh per year is deductible under Section 24(b). Your effective rate on a home loan could be 6–7% after tax savings. That makes prepaying it even less urgent.

When snowball makes sense

One case where snowball is the right call: when you're carrying several very small loans.

Three ₹15,000 BNPL balances, two fintech app loans, each with a separate NACH debit — that's five autopay mandates and five different apps to track. Closing the small ones first (snowball) simplifies your financial picture fast. Fewer loans. Fewer due dates. Less cognitive overhead.

Once you're down to 2–3 loans, switch to avalanche and focus on rate.

Hybrid approach: clear anything under ₹25,000 first. Then avalanche everything else.

What to do with a bonus

You've got ₹75,000 sitting in your account after appraisal. Which loan does it go into?

Put it on the highest-rate outstanding balance. If that's a credit card, reduce it or close it entirely. The math is clear — eliminating 40% APR debt is worth more than two extra EMIs on a 9% loan.

Before prepaying a personal loan, check the foreclosure clause. Indian banks typically charge 2–4% on fixed-rate personal loans. At 16% APR with 4% penalty, prepayment still makes sense if tenure remaining is over 18 months.

Floating-rate home loans are different: RBI guidelines prohibit prepayment penalties. You can prepay any amount, anytime, penalty-free.

Before you can prioritise, you need one number

Most people don't know their actual monthly EMI total until salary hits and the money disappears. SBI YONO shows the home loan. HDFC app shows the car loan. Bajaj Finserv shows the personal loan.

Kedil consolidates all your EMIs in one place. Add each loan once — outstanding balance, monthly EMI, interest rate, remaining tenure. See your combined monthly debt commitment without opening four apps. That number — your real total — is where any payoff plan starts.

FAQ

Should I prepay my home loan or personal loan first?

Personal loan, in almost every case. Home loan rates (8.5–9.5%) are roughly half what personal loans cost (13–22%). Prepay the personal loan first. Let the home loan run — especially if you're claiming the ₹2 lakh Section 24(b) deduction.

Is a prepayment penalty worth paying?

Usually yes, if more than 18 months remain. A 4% one-time fee to stop paying 18% saves you money from around month 8 onwards. Calculate the break-even before you act.

What's a healthy EMI-to-income ratio?

Under 40% of take-home. If you're above that — and running 5 loans — focus on closing the highest-rate one before taking any new debt.

Credit card or personal loan — which goes first?

Credit card. 36–48% APR versus 13–22%. The avalanche method gives a clear answer here.

Does Kedil help me track which loan to close first?

Kedil shows all your active loans in one view — balance, rate, EMI, tenure. Once you can see the full picture, the priority order becomes obvious. Free during early access.

Try Kedil — free during early access. Add all your loans and see your real monthly EMI total in one place. → kedil.money